Economic & Housing Weekly Note...

- Charles "Skip" Geiser

- Jul 28, 2021

- 4 min read

Housing Demand Remains Strong Despite Limited Supply and Higher Home Prices

July 23, 2021

Key Takeaways:

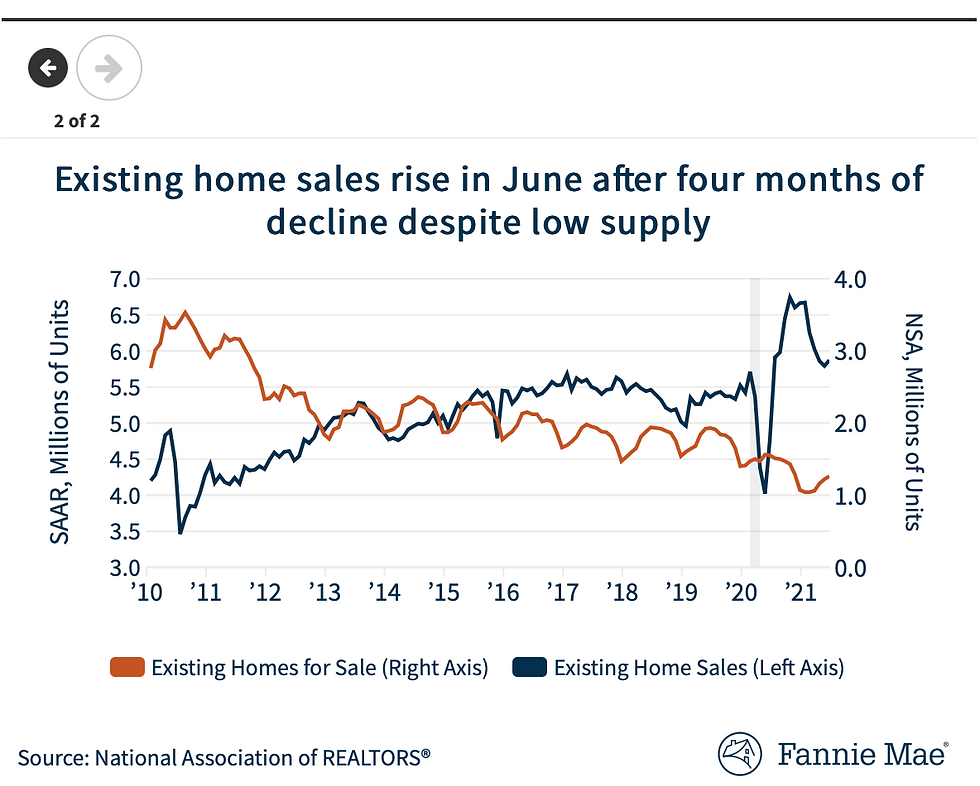

Existing home sales increased 1.4 percent to a seasonally adjusted annualized rate (SAAR) of 5.86 million in June, the first monthly increase since January, according to the National Association of REALTORS®. Single-family and condos/co-ops sales both rose 1.4 percent. Total existing sales in June were 2.8 percent above the level seen in February 2020. The number of existing homes on the market grew 3.3 percent to 1.25 million not seasonally adjusted, the highest level since November 2020 but 18.8 percent lower than last June. The months’ supply ticked up one-tenth to 2.6, the highest level since September 2020, but the lowest reading on record for the month of June. The median sales price for an existing single-family home jumped for a fifth consecutive month to $370,600, a 3.9 percent increase from May and a 24.4 percent increase from a year ago. On a quarterly basis, total existing home sales fell 7.5 percent to a SAAR of 5.83 million in the second quarter.

Housing starts increased 6.3 percent in June to a SAAR of 1.64 million, according to the Census Bureau. Excluding the March rebound following February’s cold weather and power outages, June starts were the highest since December 2020 and were evenly balanced between single-family, which rose 6.3 percent to a SAAR of 1.16 million, and multifamily, which grew 6.2 percent to a SAAR of 483,000, the highest level since July 2020. Single-family permits declined by 6.3 percent to a SAAR of 1.06 million, the lowest level since August 2020, while multifamily permits dropped 2.6 percent to a SAAR of 535,000 million, the lowest level since December 2020. On a quarterly basis, single-family starts fell 4.5 percent to a SAAR of 1.10 million in the second quarter, while multifamily starts rose 4.6 percent to a SAAR of 464,000.

The National Association of Home Builders/Wells Fargo Housing Market Index fell 1 point to 80 in July, the lowest level since August 2020, though still higher than any pre-pandemic recording since the survey began in 1985. A reading above 50 indicates that more builders view the single-family market as “good” rather than “poor.” Traffic of prospective buyers dropped 6 points to 65, the largest monthly decline since April 2020. The index for present sales declined 1 point to 86, while the index for sales in the next six months ticked up 2 points to 81. The press release mentioned that “builders are contending with shortages of building materials, buildable lots and skilled labor as well as a challenging regulatory environment”.

Forecast Impact:

June’s increase in housing starts was somewhat smaller than expected, while the decline in new building permits was larger. As corroborated by the release of the July Housing Market Index, supply chain disruptions, high lumber costs, and labor scarcity appear to be continuing to hold the pace of home construction below its full potential. Permits in June fell for the fourth time in five months, with the aforementioned constraints likely leading builders to hold off on submitting new permits until these dynamics improve. Though we continue to forecast a long-run acceleration in housing starts as builders catch up with years of pent-up demand following a decade of under-building, our near-term forecast of housing starts will likely be revised downward modestly to reflect the most recent data.

While housing starts were weaker than expected, existing home sales were stronger. Given that the traffic of prospective buyers for new homes remains above pre-pandemic levels, as well as the increase in June existing home sales, homebuying demand appears to remain robust. The June increase will likely result in an upward revision of our near-term forecast of existing home-sales, though we believe home sales are still cooling from their red-hot pandemic highs, and we still expect sales will fall in Q3. While we expect that homebuying demand will likely remain elevated as interest rates dip back to near-historic lows, the lack of homes available for sale and continued construction difficulties will likely continue to exert upward price pressure, pushing some would-be homebuyers out of the market.

Ricky Goyette and Nathaniel Drake Economic and Strategic Research Group July 23, 2021

Opinions, analyses, estimates, forecasts and other views of Fannie Mae's Economic and Strategic Research (ESR) Group included in these materials should not be construed as indicating Fannie Mae's business prospects or expected results, are based on a number of assumptions, and are subject to change without notice. How this information affects Fannie Mae will depend on many factors. Although the ESR group bases its opinions, analyses, estimates, forecasts and other views on information it considers reliable, it does not guarantee that the information provided in these materials is accurate, current or suitable for any particular purpose. Changes in the assumptions or the information underlying these views could produce materially different results. The analyses, opinions, estimates, forecasts and other views published by the ESR group represent the views of that group as of the date indicated and do not necessarily represent the views of Fannie Mae or its management.

Charles "Skip" Geiser

SkipSOLDMyHome.com with

Plum Tree Real Estate Marketing

850.221.6442

Start

Cary Schmidt's Introduction of Done

Gulf Coast Baptist Church Links

Comments